Transmedics Is Transforming The Organ Transplantation Industry

And doing so at a staggering pace!

Disclosure: As of the time of writing, I own a position in Transmedics. I may make trades in this stock in the future and my work here should not be taken as financial advice but rather for informational purposes.

I could write a lot more, but I have chosen not to info dump in here and instead touch on the most important points

You might not know this, but the organ transplantation industry is terribly outdated. Despite organ transplantations being supply constrained, we don’t seem to have taken any care to maximise the utility of these donated organs.

The Problem

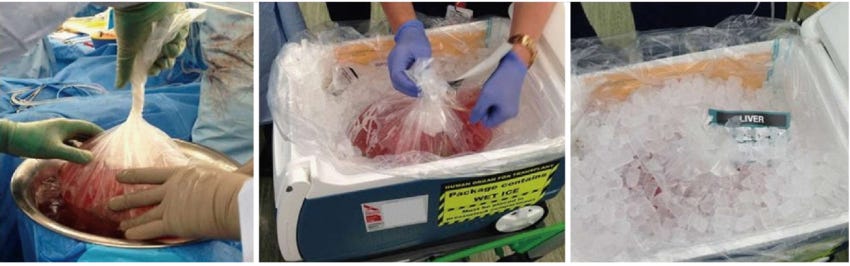

A massive number of organs are lost in transit every year, and we use a method to store organs called “SCS - Static Cold Storage” - A really high tech name for putting organs on ice in a cooler box (the same you use to store iced beverages).

Clearly, while SCS is the industry practice, it comes with a host of limitations:

1) Cold Ischemia

Organs last only for a short period of time on ice, as short as 2-4 hours for Lungs, 4-6 hours for Hearts, and 12-18 hours for Kidneys.

This narrow window to conduct transplantations while organs are still usable means a much smaller radius for organ matching (It takes time to deliver an organ from donor to patient), and gruelling hours for surgeons, (it is not uncommon to get a call in the middle of the night and be told that an organ is suddenly available for transplantation). And it wasn’t uncommon for hospital surgeons to fly to donors to first ensure the viability of these organs, further increasing their workload. Consequently, hospitals experienced high turnover from burnt out surgeons, and poor unit economics from the poor utilisation of doctors (given the ad-hoc nature of transplants), as well as from having to pay overtime.

2) Lack of Organ Assessment

Organs on ice are obviously not functioning, meaning it is much tougher to assess if there is something wrong with it. This makes surgeons much more risk adverse when it comes to the selection of organs - you don’t want to figure that there are issues with it mid-transplant. This brings us then to the subject of DBD (Donation by Brain Death) and DCD (Donation by Circulatory Death). Donors are classified under one of the two, obviously dependent on the way they passed. Under SCS, almost no surgeon would be willing to utilise organs from DCD donors. Why? When a patient dies by Circulatory Death, ie. the heart stops beating, there is a period of time that has to pass before brain activity ceases and death can be certified. This extended time period where organs are starved of blood flow and oxygen makes them highly risky for transplantation after. There has been a new practice that some hospitals are leveraging called NRP (Normothermic Region Perfusion) where after a DCD patient passes, doctors wait 5-7 mins before opening the chest to restart circulation, but clamping the arteries to the brain, to prevent brain activity. Now as you can imagine, this is a significant ethical debate within the medical community.

Some analysts from the street were concerned with the threat posed by this new approach, due to it costing ¬$13k, far below OCS, but ultimately there have been hospitals who have banned NRP. More crucially, management has stated their belief that NRP is only suitable for very niche cases (short distance drives from donor to patient), and even then NRP comes with the tendency of saving one organ, but damaging the rest and rendering them unusable.

3) Lack of Organ Optimisation

The inability to optimise organs through therapeutic intervention (replenishment of substrates, hormones) typically results in higher rates of post-transplant complications.

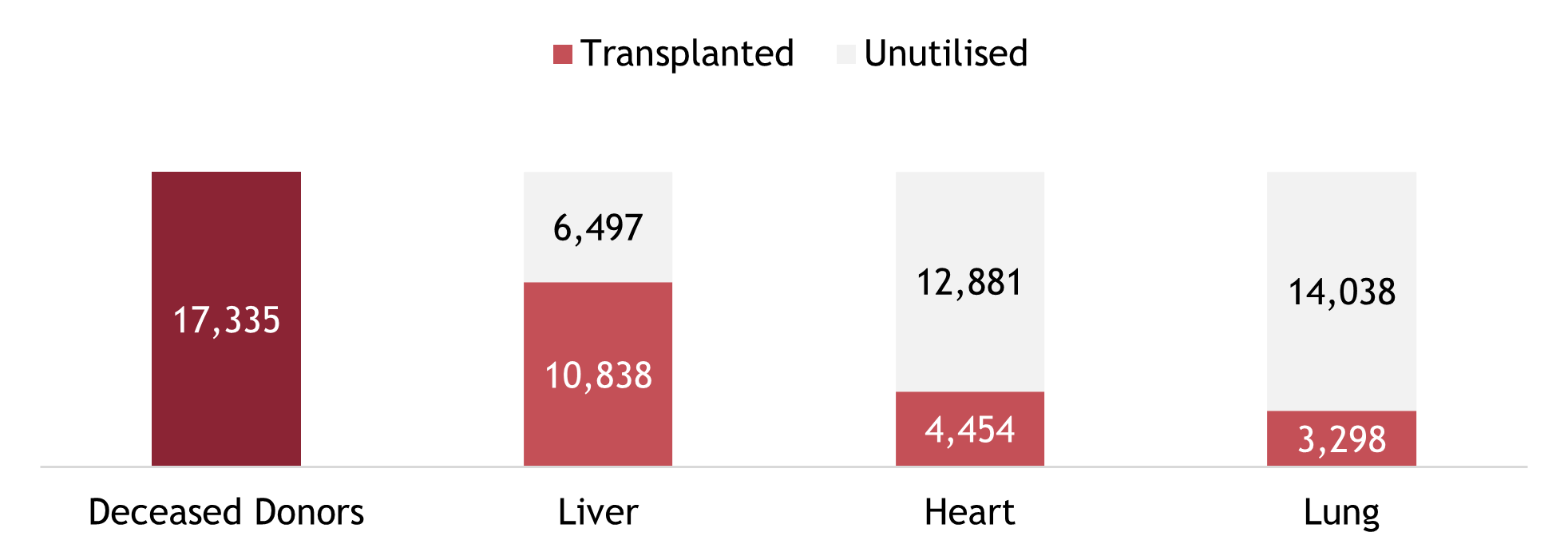

With these 3 key limitations, only 20-30% of donated lungs/hearts are used for transplantation, and 30-35% of patients experience post-transplantation complications.

The Solution

This is where Transmedics comes in with their OCS (Organ Care System) solution. A machine that keeps organs functioning outside of the human body: The Lung is breathing, the Heart is beating and the Liver is producing bile.

With OCS, distance is effectively no longer a criteria in donor matching. There aren’t stated limits on how long you can keep organs on the machine before it is unusable, but there have been organs kept on OCS for as long as a week with no increased risks of post-transplantation complications.

Now obviously, the low hanging fruit here would be the organs from DCD donors that were traditionally unusable.

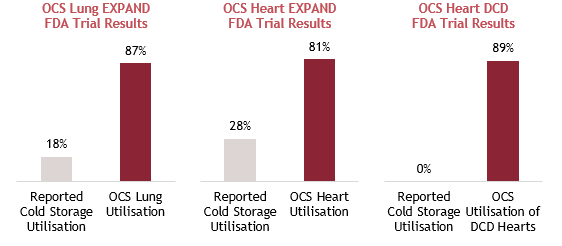

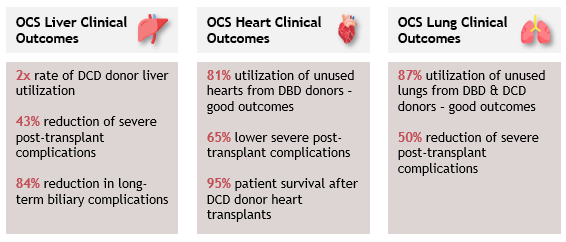

With OCS, there were some studies that Transmedics has done to showcase much higher utilisation rates across DBD and DCD donors. But even more crucially, despite utilising organs that were deemed as lower quality under SCS, OCS was able to pose much improved post-transplantation outcomes, illustrating the potential of OCS.

FDA approvals were granted in 2018 for Lung and 2021 for Heart and Liver, with over 400 patents registered to date.

Pricing Structure

Console (Free) + Consumables (¬$60k) + Services (¬$20k) + Logistics (¬$25k) = Maximum ASP of ¬$105k.

Value Chain

When one looks across the entire value chain, it is quickly clear Transmedics is one of the most compelling cases where all other parties benefit.

Patients: Safer transplants (from less fatigued surgeons), reduced risk of post-transplantation complications

Doctors: Regular working hours rather than ad-hoc, lesser cases of burnt out

Transplant Centers: Better unit economics from being able to stack transplantations throughout the day (improving surgeon utilisation rates), and from not having to pay overtime. Benefitting also from a favourable reimbursement policy where they are reimbursed on a “reasonable cost basis”, with no reimbursement cap

Payors: Huge cost savings as it is much cheaper from their perspective to provide reimbursement to get transplants done rather than using machines to keep patients suffering from last stage organ failure alive. For context, studies indicate that the cost of adding one quality-adjusted life year is roughly $40,000 (2016 dollars) for a heart transplant, compared to $800,000 for an LVAD (left ventricular assist device, or “heart pump”) for end-stage heart failure patients.

Competitive Dynamics

Notable competitors include OrganOx and Xvivo.

OrganOx: UK-based with a product called Metra that similarly to OCS, continuously perfuses donor livers with oxygenated blood. However, the product is nascent, is only for liver, and not compatible with air transport

Xvivo: Swiss-based with a product called XPS, the first FDA-approved device for ex vivo lung perfusion. However, the system is bulky and not suitable for transportation. They also compete in the kidney transplant market and is in pre-market approval for liver in the U.S.

While competitors appear to be more nascent, with the lack of portability and shorter organ survival times, more crucial was the commentary given by Xvivo’s CEO stating that he believes the market opportunity is 100x larger (10x more value and 10x more volume), and also mentioned needing players like Transmedics to help educate and grow the market.

Investment Thesis

Short and Long Terms Beats in Revenue

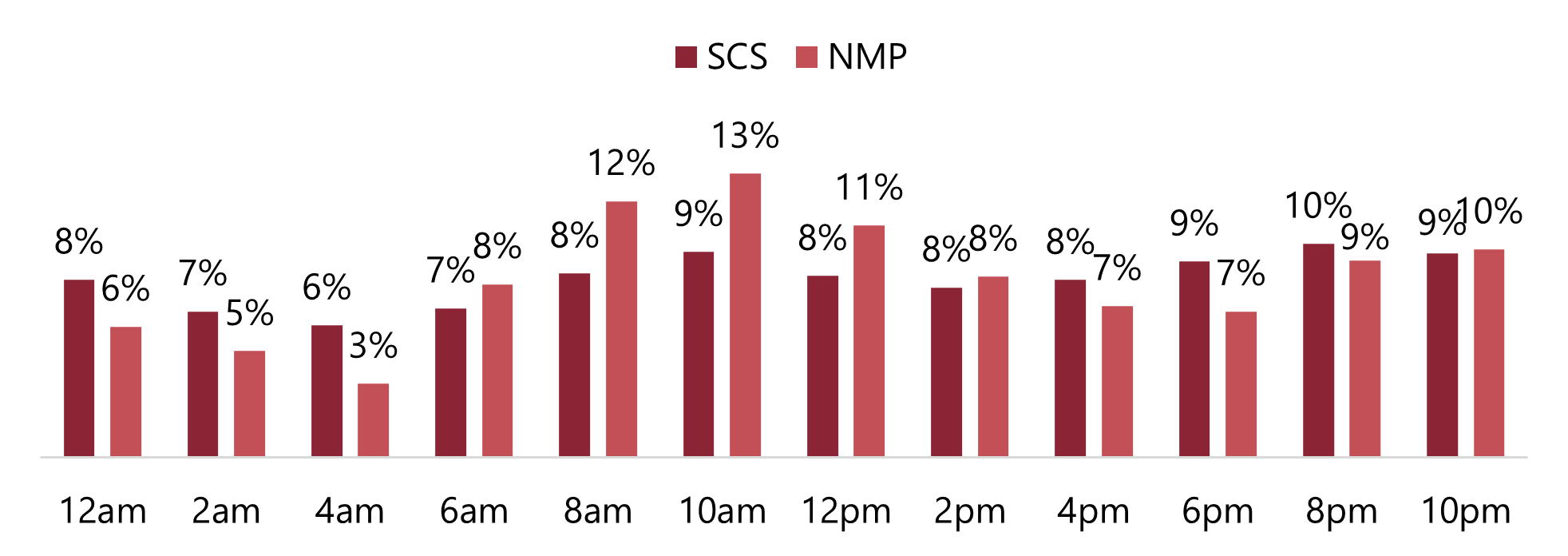

By tracking the flights of Transmedics’ aviation arm, I was able to correctly predict sequential growth closer to 15% rather than the 3% expected by the street, by observing flight frequency data.

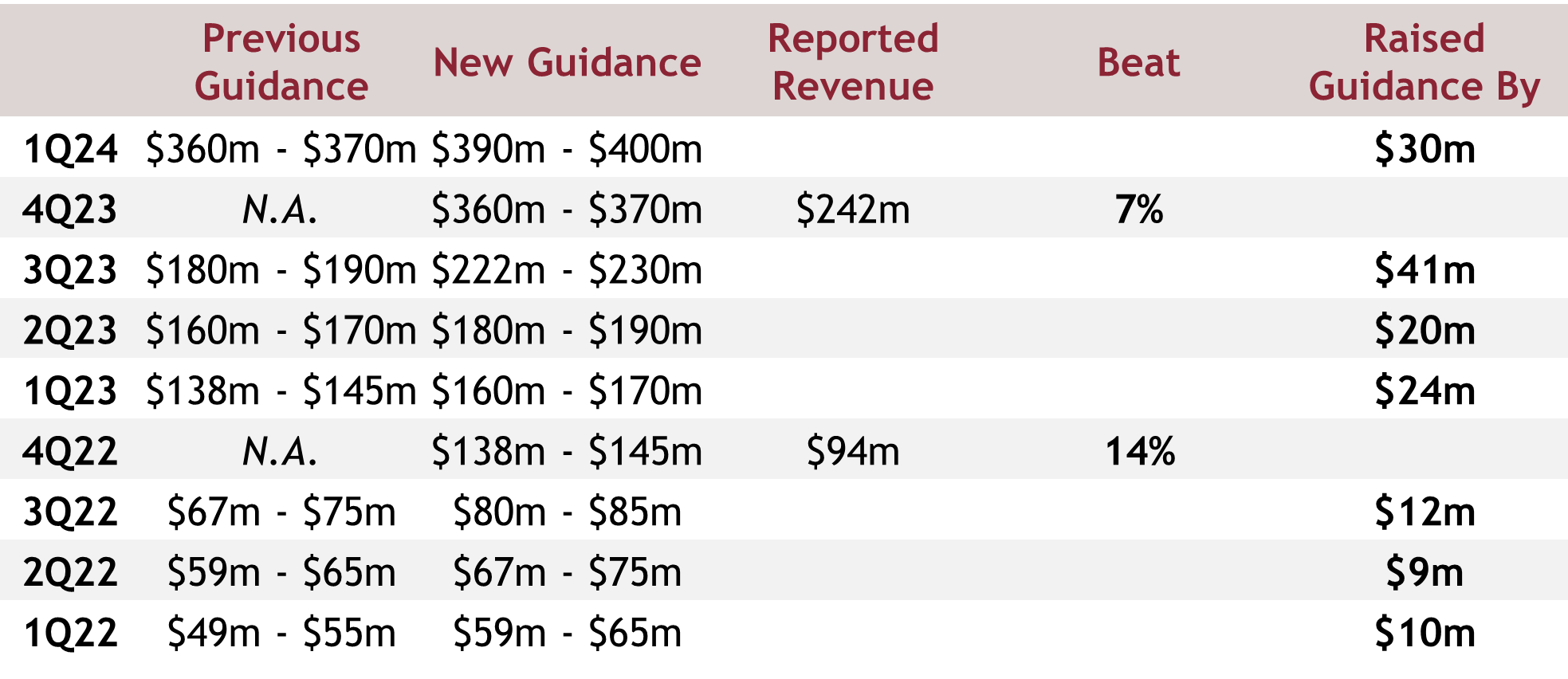

Management historically has a tendency to sandbag guidances, with repeated beat and raises demonstrated over multiple quarters.

The latest guidance of $425m implies flat sequential growth for the next quarter, and it is still difficult to predict how the quarter will play out, given we only have July’s data points for now, though July was sequentially down from June (but so was the number of organ transplants in the industry).

What is for sure though, is that the long term growth trajectory of the company is still being severely underestimated. Management has set the goal of 10,000 transplants in U.S. by 2028, and a quick look at the street’s long term revenue estimates suggest that they do not believe this will happen. Now, this is surprising given the consistency in messaging from management, constantly echoing the target of 10,000 transplants, and reiterating 10,000 would only represent a portion of the addressable market.

Long Term Margins May Be More Accretive Than Expected

Management thus far has not disclosed much metrics on the aviation arm, and their practice of lumping Aviation/Logistics under Services have led many on the street to notice that Aviation/Logistics is actually margin accretive. By backsolving for margins using several disclosed figures, I estimate Logistics to have GP margins of ¬45% vs ¬30% for Services. This implies that as the Logistics arm of the business continues to scale (with higher utilisation of aircrafts and further aircraft acquisitions), the overall margins of the Services business should expand more than what the street is expecting.

Key Growth Levers in Kidney and International Markets Remain

Management has stated a desire to enter the Kidney market once they have addressed the sluggish growth Lung OCS is facing. The market opportunity for Kidneys is far larger than the other 3 organs given the sheer number of transplants that are being done. I suspect it was initially put off due to Kidney having longer ischemic times (48 hours) compared to the other organs, making it less of an urgent solution.

It goes without saying that the number of transplantations outside of the U.S. is far larger, and conversely, so is the opportunity. What stands in the way however, is reimbursement approvals, which Transmedics is currently working to obtain. Again, these reimbursement approvals are crucial for the unit economics of transplant centers and scaling OCS outside of the U.S. will be tough with reimbursements. I do believe however, that the probability of securing those are extremely high given the huge cost savings that payors gain from enabling these end-stage organ failure transplants to be done, though there has been no commentary on timelines that management has given yet.

Valuation

I have since updated my rather elaborate valuation model (which I have chosen not to show) following the Q2 earnings report but will boil down my assumptions here. I have derived a target price of $221.51 with an implied upside of 29.7% and 5-year IRR of 18.5% with the following assumptions.

WACC: 11.8%

Revenue Forecasts:

FY24: $465m

FY25: $704m

FY26: $911m

FY27: $1,095m

FY28: $1,251m

EBITDA Forecasts:

FY24: $67m

FY25: $146m

FY26: $233m

FY27: $334m

FY28: $442m

EBITDA to FCF Conversion Assumptions:

FY24: -269%

FY25: 35%

FY26: 53%

FY27: 62%

FY28: 67%

Exit Multiple Assumptions:

EV/Rev: 8.8x

EV/EBIT: 30.6x