Meituan: The epitome of laziness

Deriving 30% to 62% upside with 5-year 20%+ CAGR expected in operating profits while trading at 13x NTM EV/EBITDA

Happy 2025! Previously many of my writeups were often general dives into businesses that I was interested in looking into - which meant they weren’t necessarily actionable. In 2025 I will attempt to have more actionable ideas and be clear at the beginning of the writeups as to whether its a investment idea or a general dive into a company. Now time is often the essence for investment ideas and this means they will tend to be a shorter form.

This writeup on Meituan will be an investment idea with an upside of 30% to 62%. Disclosure: I currently own a position in them but may sell without notice.

There is a high possibility China is back. Sentiment has sharply changed from Deepseek and there has likely been overblown fears over US China relations. China has recently entered a bull market and if you were to zoom out, multiples are still comparatively cheap.

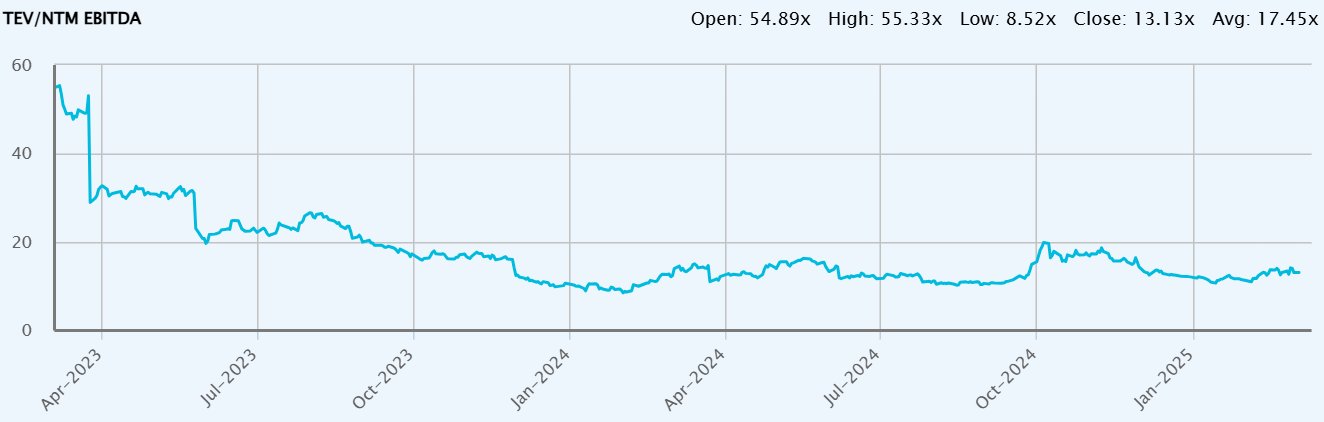

If you were active on Fintwit, you would have seen the recent craze over Grab. Yet this chart presents Meituan as a much more compelling opportunity.

So let’s talk about Meituan and food delivery in general. Meituan has a near-monopoly position in China’s food delivery market, with market share of more than 70%.

The number of transacting users reached 753 million in 2Q24, making it one of the largest apps in China. Meituan’s service offerings largely cover all types of services essential to daily life in China, including food (food delivery and restaurant booking/deals), travel (hotel booking, plane/train tickets, tourist site tickets), household maintenance services (cleaning, plumbing, electricians), entertainment (escape room, karaoke, board game cafes, theme parks), tutoring and classes (gyms, sports, music instruments, languages) and many others.

Scale in food delivery is everything unlike ride hailing. In food delivery, scale enables you to do something called order batching - that is a rider picking 3-4 orders within a small radius, then heading out to deliver them, drastically improving unit economics. This is not something that can be achieved in ride hailing (ride sharing exists on a limited scale because no one wants to continuously stop for other passengers).

As a result, once scale is achieved, it is typically near impossible for nascent competitors to leapfrog incumbents in market share. This observation is consistent with Grab, DoorDash and Meituan.

There remains plenty of room for penetration rates and margin expansion in the future. Bear in mind they are delivering 20% growth in what is perceived as a sluggish China economy, while their profitability inflection is underway. There is a high possibility we see operating profits compound at 20%+ CAGR over the next 5 years. Additionally, with stimulus from China underway, we could see a reacceleration in GDP growth, which would not only boost Meituan’s financials, but also provide another leg of multiple expansion given that it would feed into the changing sentiment in China equities.

And unlike the rest of the world, China outbound tourism has not recovered with the same rigour as the rest of the world. According to China Trade Desk, around 128 million Chinese travelers will venture abroad in 2024, far off the pre-pandemic peak of 155 million but expects China’s outbound travel hitting 200 million by 2028. This will benefit Meituan because they also operate a online booking services for hotels, flights and train tickets, and tickets for tourist sites (Think Trip.com).

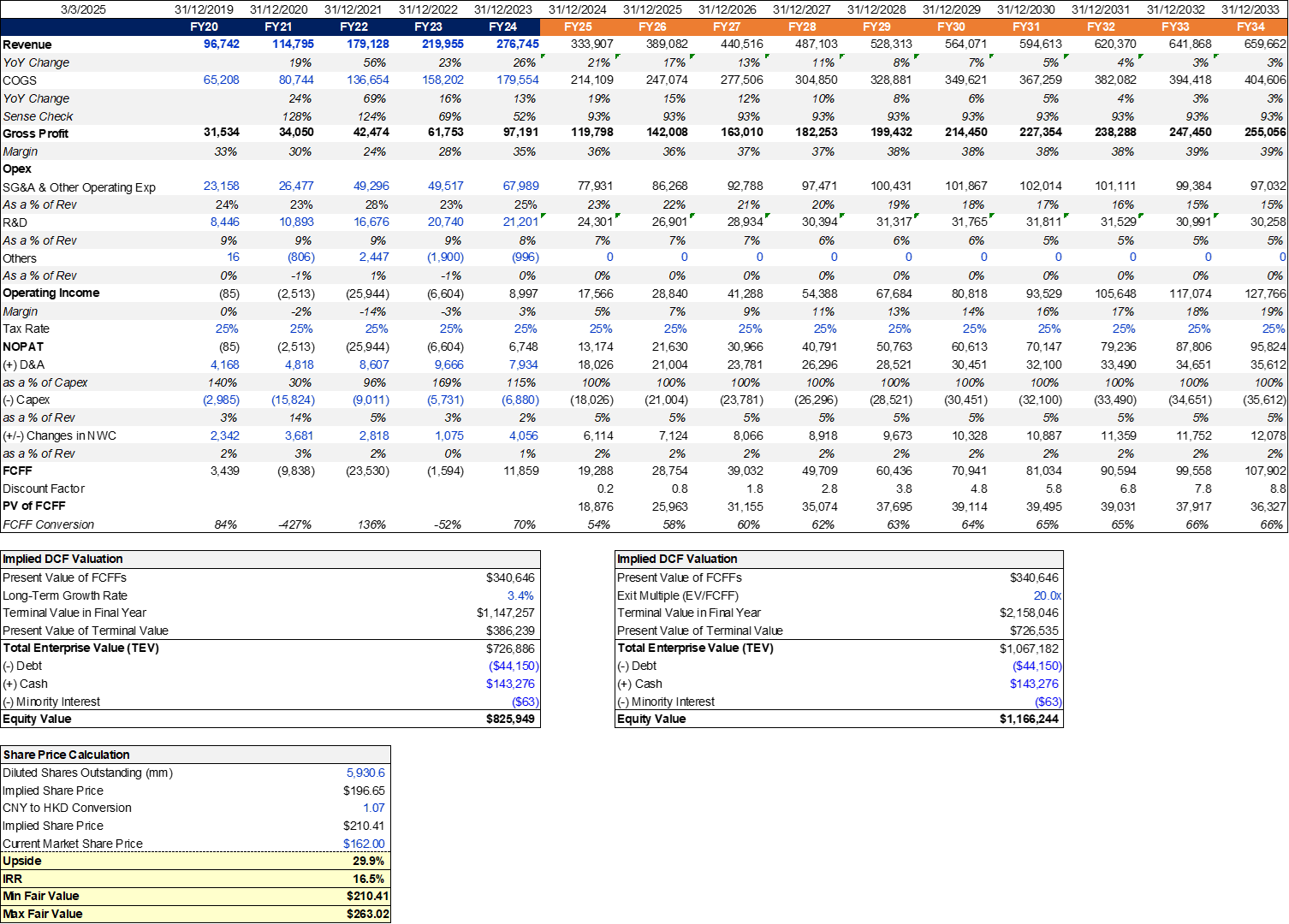

Valuation

My fair value range for Meituan is $210 to $263, with implies upside ranging from 30% to 62%. Key drivers of share price growth would be 20%+ CAGR growth in operating profits, with a degree of multiple expansion from improved China sentiment which would be the icing on the cake.

Additional Notes: Meituan YTD performance has lagged other China internet peers (BABA, PDD etc), which provides better risk reward. Also, I personally prefer a domestic play on China because they would not be as exposed to policy risk from US.