Genda Caught My Eye

They are getting IRRs as high as 144%!

Disclosure: As of the time of writing, I do not own a position in Genda. I may make trades in this stock in the future and my work here should not be taken as financial advice but rather for informational purposes.

Before I get into this, I do have to credit Made In Japan for the original writeup on Genda $9166. I came across the piece and decided to look more into the company. The full writeup done by Made In Japan can be found here:

Genda is a really interesting company that certainly has things going for them - see my thoughts below (I have way too many but too little time so I chose to zoom in on a few) to learn more about them.

There are several tailwinds for serial acquirers in Japan.

Extremely low interest rates

Ageing business owners with no potential successors

Poor financial literacy resulting in attractive multiples for acquisition targets

Genda is an entertainment company that acquires businesses predominantly in the arcade industry (like claw machines, not gambling), though they have acquired karoakes and other entertainment related businesses too (32 M&As to date). Having spoken to management, you can sense that the management strictly follows a returns driven approach, and is more than willing to branch into other industries in pursuit of investment opportunities with high returns.

They have an equity hurdle rate of 10% for their investment considerations, though frankly they might as well not have it. They have been able to acquire businesses for as low as 0.1x to 5x EV/EBITDA (both extremes are rare) on a post PMI (Post Merger Integration) basis, and have done IRRs in the 3 digits on some investments (which was what caught my attention!). Most acquisitions will land somewhere at 3.5x EV/EBITDA and management has indicated these multiples remain achievable for the next few years. The pipeline for deals remain strong, currently at 99 vs 170 last year with plenty of deal opportunities still on the table.

Management has hinted that there will be a shift towards larger sized deals, and has also hinted at an equity based deal that will probably happen in 2H 2024 (they just did a secondary offering today which lines up), as long as the acquisition is EPS accretive - again they are very returns driven with a good understanding of capital allocation. I do appreciate their transparency with disclosures - they are definitely much more investor friendly than the average Japanese corporation. Look at them going out of their way to run a math class to showcase the benefits of accretive M&A deals which I found amusing.

Financial literacy for M&A in Japan is much lower compared to areas like US, and this presents an opportunity for Genda. To further illustrate the attractiveness of these acquisition multiples: Opening a store would cost roughly 200m yen in capex. Genda has been able to acquire 14 businesses with that same amount.

Their PMI measures include renovating and introducing prize based games (claw machines with anime prizes). This is where some economies of scale is achieved by bulk buying prizes.

Price per game is capped at 1,000 yen due to regulation. What is worth noting is RoundOne did try raising prices and failed.

On pricing there is an interesting dynamic - Genda raised prices to 200 yen per game, but also made the game easier to win. The resulting outcome is that though the payout is the same, customers feel better (they win quicker) and come back more often. But crucially this also enables customers to get in and out quicker, which increases the number of individuals that get to play.

80% of stores are cashless - which are superb for making consumers overspend given the intangible nature of payments. Most of the machines were cashless as SEGA previously spent the capex to revamp the payment modes. Doing so is typically pretty capex intensive and most competitors are unlikely to follow suit. Genda themselves do not expect that 80% to increase - the remaining 20% are typically in suburban areas and there is no real need to do so.

Where my concern lies

Maintenance capex is 5% of revenue.

Napkin math tells me this: Assuming they acquire businesses for 3.5x EV/EBITDA straight cash (supposedly the rough average of their acquisition multiples), that gives an IRR of ¬29%.

If EBITDA margins of these companies are 13% (roughly in line with historicals), that effectively gives you a 5.7x EV/(EBITDA-Capex) multiple (proxy for FCF), which now yields you a less attractive IRR of 18% assuming its a straight cash deal.

But if you were to assume that their sources consist of 1x Equity and 2.5x Debt to remain below that Net Debt/EBITDA ceiling, they should get a ballpark equity IRR of 62% (Yes, I didn’t account for interest so it will be slightly lower but not that material given that interest rates are slightly above 1%.)

Net debt has increased significantly to 1.8x of EBITDA (as it should because that’s the play - take lots of debt and get great IRRs), but management has said 3x is the absolute ceiling and they do not expect banks (who are their financiers) to be comfortable with them getting close to 3x. The real ceiling is likely to be closer to ¬2.5x. This will mean either slower M&A activity or more equity deals.

Looking at Tier 1 serial acquirers (Constellation Software, Lifco), capex spend for them has been around 10% of operating cash flow. With Genda, this is closer to 50%. What is clear to me is that without a constant increase in leverage, the sustainability of acquisition spend is in doubt owing to a high proportion of cash flows going over to maintenance capex spend.

Valuation

Valuing a company whose growth is dependent on acquisitions will always be trickier - it is difficult to estimate the multiples that they will pay for as well as the incremental EBITDA that is added.

The key assumptions used in my computation were:

8% organic growth in the first fiscal year for existing and newly acquired businesses, followed by 1% annually for the next 4 years. This is to factor in the relatively strong Same-Store-Sales (SSS) growth that they have experienced thus far, and also to factor in their string of successful PMI implementations for their acquisitions.

M&A spend of 21b in first fiscal year followed by 6% growth tapering by 1% every year. Acquisition multiple of 3.5x EV/EBITDA, with an assumed EBITDA margin of 13%. This means they reach a max leverage of 2.5x Net Debt/EBITDA by FY29.

Capex spend to be maintained at 8.3% of revenue, given roughly ¬5% is for maintenance.

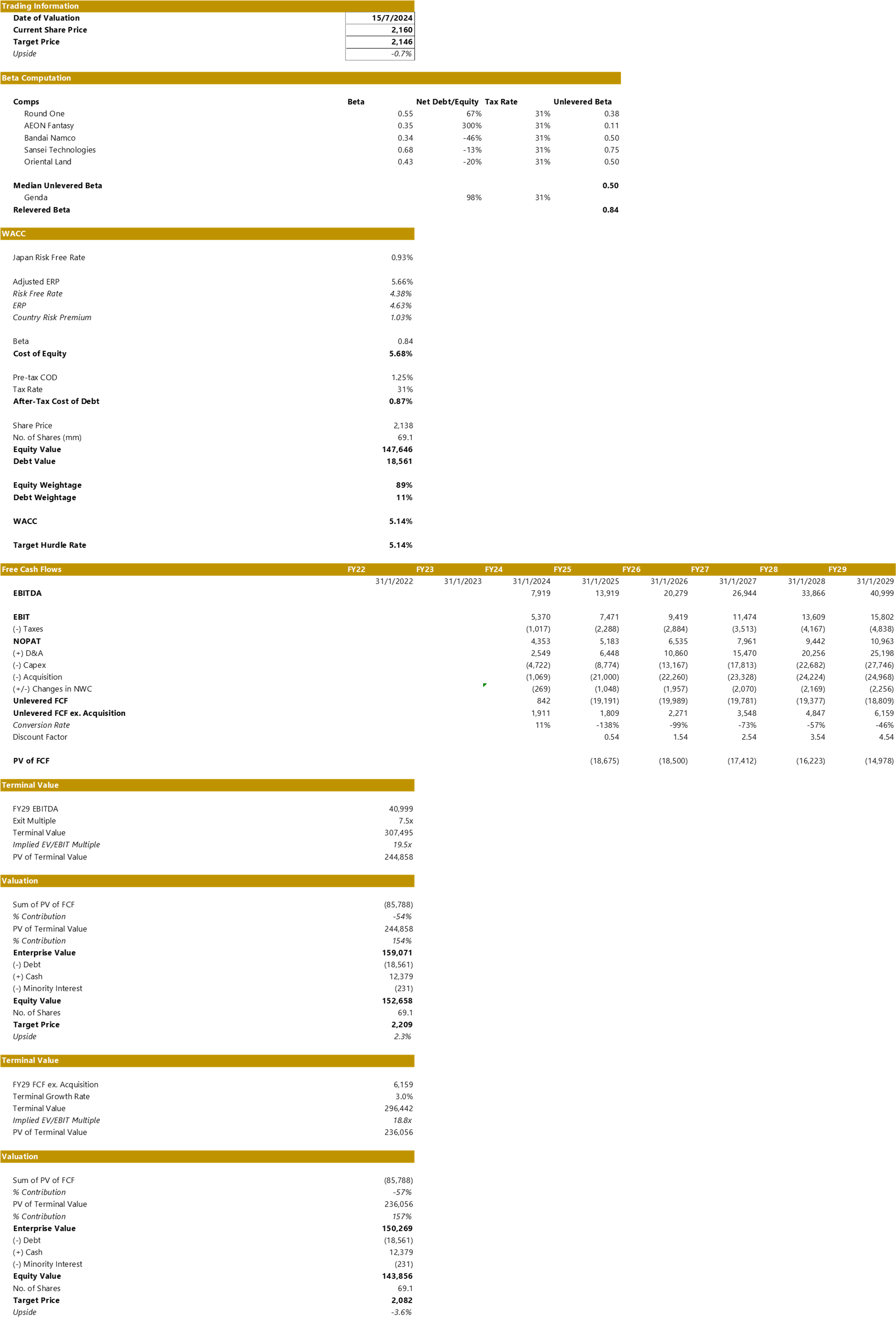

Using a WACC of 5.14%, with 3% terminal growth (implying EV/EBIT multiple of 20.7x), and using an exit multiple of 7.5x EV/EBITDA (implying EV/EBIT multiple of 19.3x), I arrived at a target price of 2,146 yen, implying a return of -0.7% over the current trading price of 2,160 yen. This is despite a pretty low discount rate (at least if you are based outside of Japan), so I find it difficult to see much upside at this point unless they surprise massively in their equity based deals. I could very much be wrong with my M&A assumptions and I will be on the lookout for shareholders reaction to their equity deals (I have seen other stocks usually sell off even though the M&A deals have been accretive)

Great research but maybe a tip as a fellow equity analyst (self employed as well managing money and publishing). I got really excited at the start but by the end you seems to indicate its perfectly priced. In the beginning I thought this research is actionable; however, I'm guessing it's not anymore. Maybe focus more on actionable publishing and make it clear with your IRR on the stock from the very begining. But great note, and would have loved to buy something like this a roll up type play if it was actionable